Key Takeaways

- Personal bookkeeping for busy families helps organize complex household finances and reduces stress.

- Many families struggle with managing multiple accounts, receipts, and reimbursements, leading to scattered financial details.

- Common signs that casual tracking is insufficient include missing receipts and unsubmitted reimbursements.

- A bookkeeper can categorize transactions, organize receipts, and prepare reports, but does not replace the need for professional advice.

- Seeking help early can bring a calmer system to your household finances and improve overall organization.

Some households reach a point where ordinary money management no longer feels ordinary. This is often when personal bookkeeping for busy families becomes essential to keep finances organized and stress levels low.

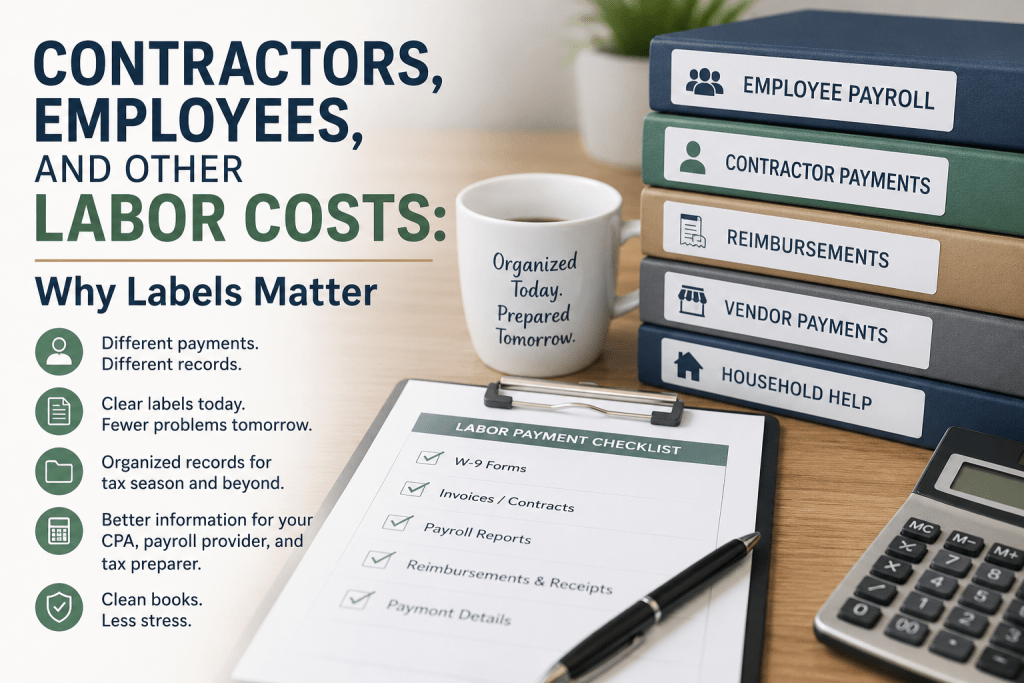

There may be multiple credit cards, debit cards for kids, recurring subscriptions, school payments, medical bills, travel expenses, charitable giving, reimbursements, and payments to household help. One parent may make business-related purchases on a personal card. Another may manage school fees, sports registrations, and household vendors. Someone else may need to track receipts, returns, or reimbursements.

None of this means the household has done anything wrong. It simply means the financial details have grown.

Many busy families reach a point where their household starts to run a little like a business. They have accounts, vendors, receipts, recurring payments, reimbursements, and records to organize. But unlike a business, the household may not have a regular bookkeeping process in place.

That is where personal bookkeeping can help.

Your household may have more moving parts than you realize

A busy household can generate a surprising amount of financial activity in a normal month.

There may be mortgage payments, utilities, insurance, tuition, activities, groceries, travel, medical expenses, gifts, charitable contributions, household payroll questions, subscriptions, and card purchases from several family members. Add business reimbursements, shared expenses, or payments to a housekeeper, nanny, caregiver, or assistant, and the details can quickly spread across several accounts.

The challenge rarely comes from one large problem. It usually comes from dozens of small details that no one has time to sort.

A receipt goes missing. A reimbursement sits unsubmitted. A subscription renews unnoticed. A child uses a debit card for school expenses. A household helper buys supplies. A business purchase lands on a personal credit card. By the end of the month, everything still shows up somewhere, but the full picture feels scattered.

The Bureau of Labor Statistics reported that, on an average day in 2024, 80% of people spent time on household activities such as housework, cooking, lawn care, or household management, averaging about two hours on those activities. For busy families, financial organization often competes with that same limited personal time. (Bureau of Labor Statistics)

The signs that casual tracking no longer works

Many families start with a simple system. They check bank balances, glance at credit card statements, save a few receipts, and pull documents together at tax time.

That may work for a while. But as life gets more complex, casual tracking can leave too many gaps.

Here are a few signs your household may need a more organized process:

You spend too much time searching for receipts.

You miss reimbursements because no one submitted the expense.

You have several credit cards, but no clear system for reviewing what each card covers.

Your children or household helpers use cards, but you do not have an easy way to categorize their spending.

You feel unsure about which expenses relate to your household, work, business, property, charitable giving, or medical needs.

You dread gathering records for your CPA or tax preparer.

You notice recurring charges but do not know which ones still matter.

You and your spouse or partner have different pieces of the financial picture.

These are not signs of failure. They are signs that your household has outgrown a casual approach.

Why bank balances do not tell the full story

A bank balance can tell you how much money sits in an account today. It cannot always tell you where the money went, which expenses need documentation, which purchases require reimbursement, or which transactions need follow-up.

Credit card balances work the same way. They show totals, but they do not explain the story behind each charge.

For example, a single credit card statement might include groceries, a child’s school expense, a business lunch, a medical copay, a hotel deposit, a charitable donation, household supplies, and a reimbursable work purchase. The total balance matters, but the categories matter too.

Without organized records, families may end up relying on memory. That creates stress because memory rarely keeps up with a full household calendar.

Good bookkeeping does not just track money in and money out. It creates a clearer record of what happened.

What personal bookkeeping can organize

Personal bookkeeping helps bring structure to the financial side of household life.

For busy families, that may include:

Monthly transaction review and categorization

Credit card and bank account organization

Recurring expense review

Household vendor payment records

Expense summaries by category

Support for gathering information for a CPA or tax preparer

Clearer reporting for household decision-making

The goal is not to make your home feel corporate. The goal is to give your household a dependable system so financial details do not take over your evenings, weekends, or tax season.

A personal bookkeeper can help you see patterns, organize records, and reduce the last-minute scramble. Instead of sorting months of transactions at once, you can maintain cleaner records throughout the year.

What a bookkeeper can and cannot do

A personal bookkeeper helps organize records and provide clear financial information. That can make household finances easier to understand and easier to share with the right professionals.

A bookkeeper can categorize transactions, reconcile accounts, organize receipts, track reimbursements, and prepare reports. A bookkeeper can also help keep records in better shape for your CPA or tax preparer.

A bookkeeper does not replace a CPA, tax preparer, attorney, financial planner, or investment advisor. A bookkeeper should not give tax, legal, investment, or financial planning advice. Instead, the bookkeeper helps organize the information those professionals may need.

That distinction matters. Clean records support better conversations, but they do not replace professional advice.

When to ask for help

You do not need to wait until your household finances feel overwhelming.

It may make sense to ask for help when your family has multiple accounts, several card users, regular reimbursements, household help, significant travel, medical expenses, business-related purchases, or a growing pile of receipts and statements.

You may also benefit from help if you value your time more than the task itself.

Some families can manage the details on their own. Others have the ability, but not the time or desire. That is a practical reason to hand off the work.

Personal bookkeeping can give busy households a calmer way to stay organized. It creates a monthly rhythm, reduces guesswork, and helps keep important records from getting lost in the pace of daily life.

Get your household records organized

If your household has multiple cards, reimbursements, recurring expenses, and records to track, Pavlovich Bookkeeping Co. offers limited personal bookkeeping to help organize records, track expenses, and provide clear information for your CPA or tax preparer.

Your household may not be a business. But it may still deserve the same level of organization.